Will A LNG Flood Lead To The Collapse Of Natural Gas Prices?

From the March 2009 issue of EEnergy Informer.

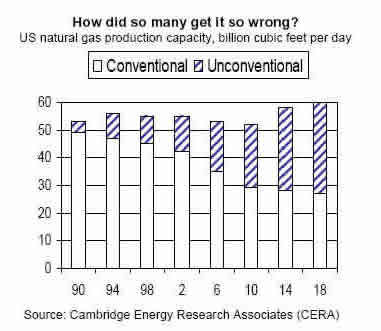

More LNG imports are likely to result in depressed US natural gas prices

As every investor knows, in any business, timing is crucial. And by that measure, the timing of many multiâ€billion dollar infrastructure investments in LNG processing, transport and receiving schemes appears to be badly off.

In the early 2000, the conventional wisdom was that the US domestic production capacity was on the decline requiring massive imports of liquefied natural gas (LNG) from overseas. With natural gas prices at allâ€time highs and projected to go even higher, a number of multiâ€national giants began massive investments in export and receiving terminals and specialized tankers that can transport the liquefied fuel from producing countries to major markets in the Pacific Rim, Europe, the east coast of the US and the Gulf of Mexico.

Now, just as these projects near completion, the demand for natural gas seems to be evaporating with the global economic recession resulting in a potential price collapse. Making matters worse, US domestic production – long dormant – has grown considerably in the recent past, further reducing the need for imports. The big surprise – something everyone missed – was that higher natural gas prices would result in investment in unconventional domestic resources, and that would make up for any drop in falling conventional resources (see graph).

Houston Chronicle (1 Feb 09), for example, reports that as many as seven new LNG export terminals are expected to begin operation this year, expanding worldwide capacity by 20% and flooding markets with new supplies just as the demand for natural gas is tapering off. Similarly, dozens of new LNG tankers are commissioned at a time when transportation demand is slacking off. The result? Significantly lower prices and dislocations in traditional shipping and storage patterns.

To appreciate the massive turnaround, as late as 2006, the Energy Information Administration (EIA) was predicting that the US imports of LNG would reach 6.4 trillion cubic feet by 2025. But the EIA’s latest Annual Energy Outlook released in December 2008 shows a peak of about 1.5 in 2018, followed by a gradual decline to 1.2 by 2025 (see graph).

Natural gas accounts for 23% of total energy consumed in the US, heating roughly half of the US homes and accounting for 20% of the country’s power generation. Imports, mostly through pipelines from Canada, account for roughly 16% of total US consumption. LNG is currently a niche market, representing no more than 3% of the US imports. EIA now projects that US LNG imports will not exceed 3% of total usage by 2030 – which suggests that LNG imports will play a marginal role.

But that is not the end of the surprising natural gas story. The real surprise is that despite the declining need for imported LNG, the US may end up on the receiving end of much of the global excess production and transportation capacity because of its massive storage. According to Murray Douglas, of Wood Mackenzie in Houston, “We don’t believe Asia and Europe will be in a position to absorb this new (LNG) production, and the U.S. is the only market that can take it, that has a large amount of storage.” He is predicting that the U.S. LNG imports will grow 30% to 456 billion cubic feet in 2009, and more than 1.1 trillion cubic feet by 2013 – simply because the stuff has no where else to go.

While one can dispute these numbers, there is now broad agreement that a US LNG import surge is coming. US LNG imports, primarily arriving through 5 receiving terminals, set a record in 2007 at 770 billion cubic feet. Three new terminals came on line in 2008, including two near Houston and one near Boston.

Another terminal on the West Coast just south of the California border in Mexico (Sempra’s LNG Bets Pay Off With Costa Azul, Jul 08) apparently has been receiving few shipments due to lack of demand.

Setting aside the need to recover massive fixed investments, the LNG itself can be sold for as low as $3 per million British thermal units (BTUs), including transportation costs. That, if one believes the experts’ predictions, may be as low as the prices could go – far below the current $4.50 per million BTUs – not seen since 2002, and far below the peak price of $13.50 last July. As they say, life is full of surprises.

Why would anybody sell LNG at such a low price? Because, as Zach Allen, head of Pan EurAsian Enterprises, says, “Some cash is better than none,†especially for low cost producers such as Qatar or for others where natural gas is a byâ€product of extracting oil.

One Response to 'Will A LNG Flood Lead To The Collapse Of Natural Gas Prices?'

Leave a Reply

You must be logged in to post a comment.

on February 27th, 2009 at 12:53 pm

[…] of natural gas is up. Macroeconomic factors are reducing demand for natural gas. And yet, as Fereidoon Sioshansi points out: The real surprise is that despite the declining need for imported LNG, the US may end up on the […]